AFG: Processor Atlas — Map the chokepoints, finance the throughputs

We’re building a living map of hemp & bamboo processors in North America. Not for vibes; for throughput. If you run a line (or want to), bring your bottlenecks. If you deploy capital, bring your term sheet. We’ll route deals through incentives so the math pencils without magical thinking.

Why this exists

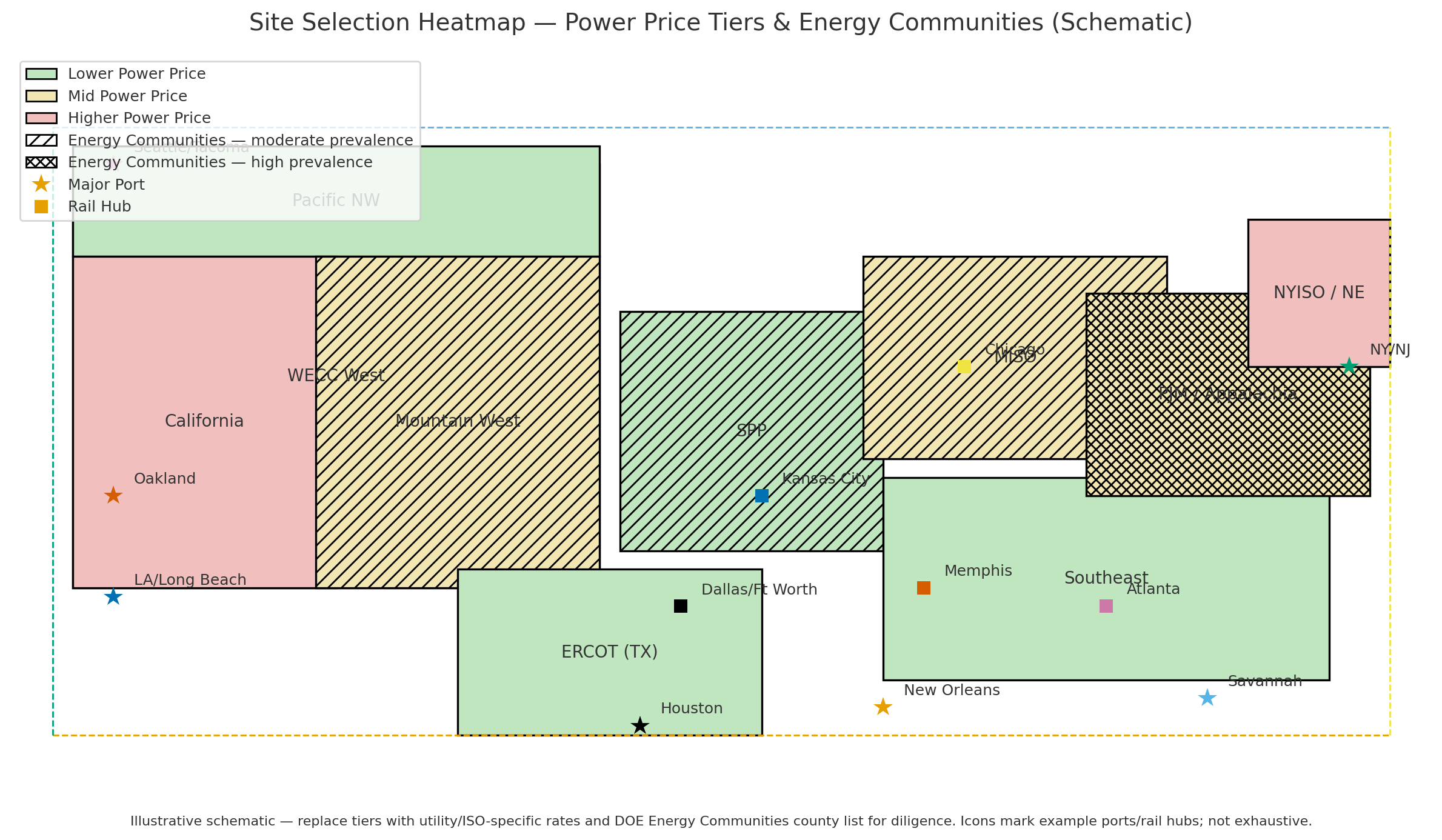

The petro stack wins with infrastructure, incentives, and narrative. So we’re answering with the same weapons—minus the greenwashing. The American Fiber Group (AFG) Processor Atlas identifies where capacity actually sits, what it can do next quarter (not 2030), and how to finance incremental throughput using the current rulebook (FEOC, Domestic Content, Energy Communities Notice 2023-29, §6417 Direct Pay, §6418 transferability, 45X/48C).

Translation: we will stop arguing in the comment section and start moving fiber.

What the Atlas is (and isn’t)

Is:

A vetted directory of processors with capabilities, constraints, and dealability.

A pipeline of throughput upgrades packaged to be financeable now.

A crosswalk to policy: which incentives apply to which upgrades—no fairy dust.

Isn’t:

A directory of growers, influencers, or “we have a deck.”

A museum of “someday” pilot projects.

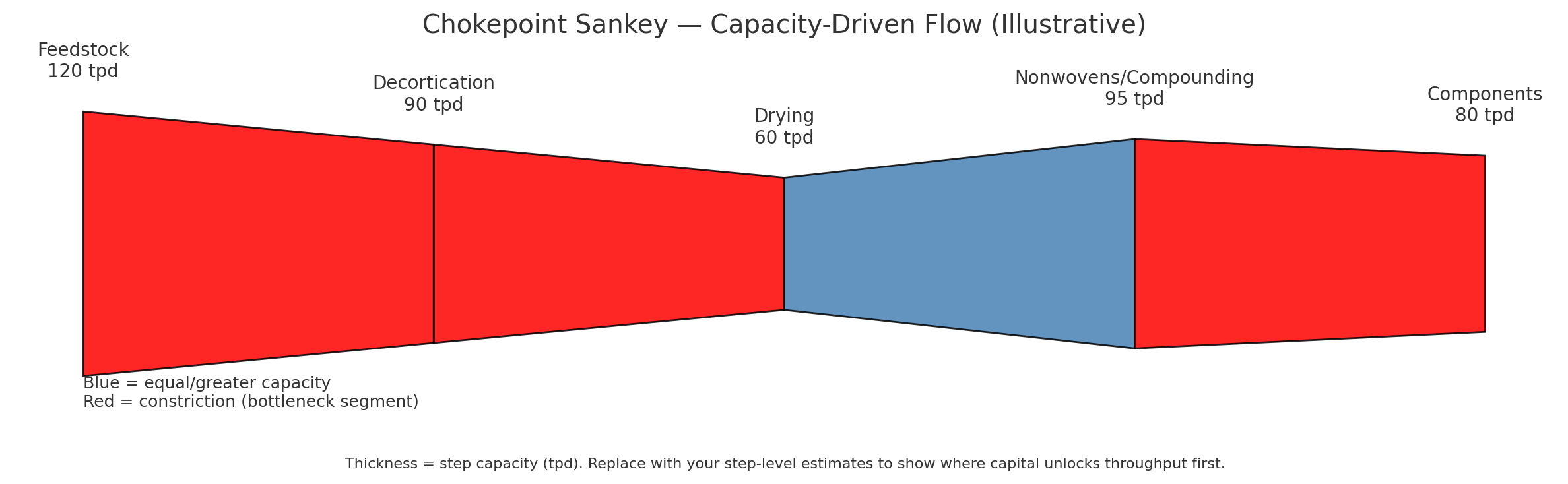

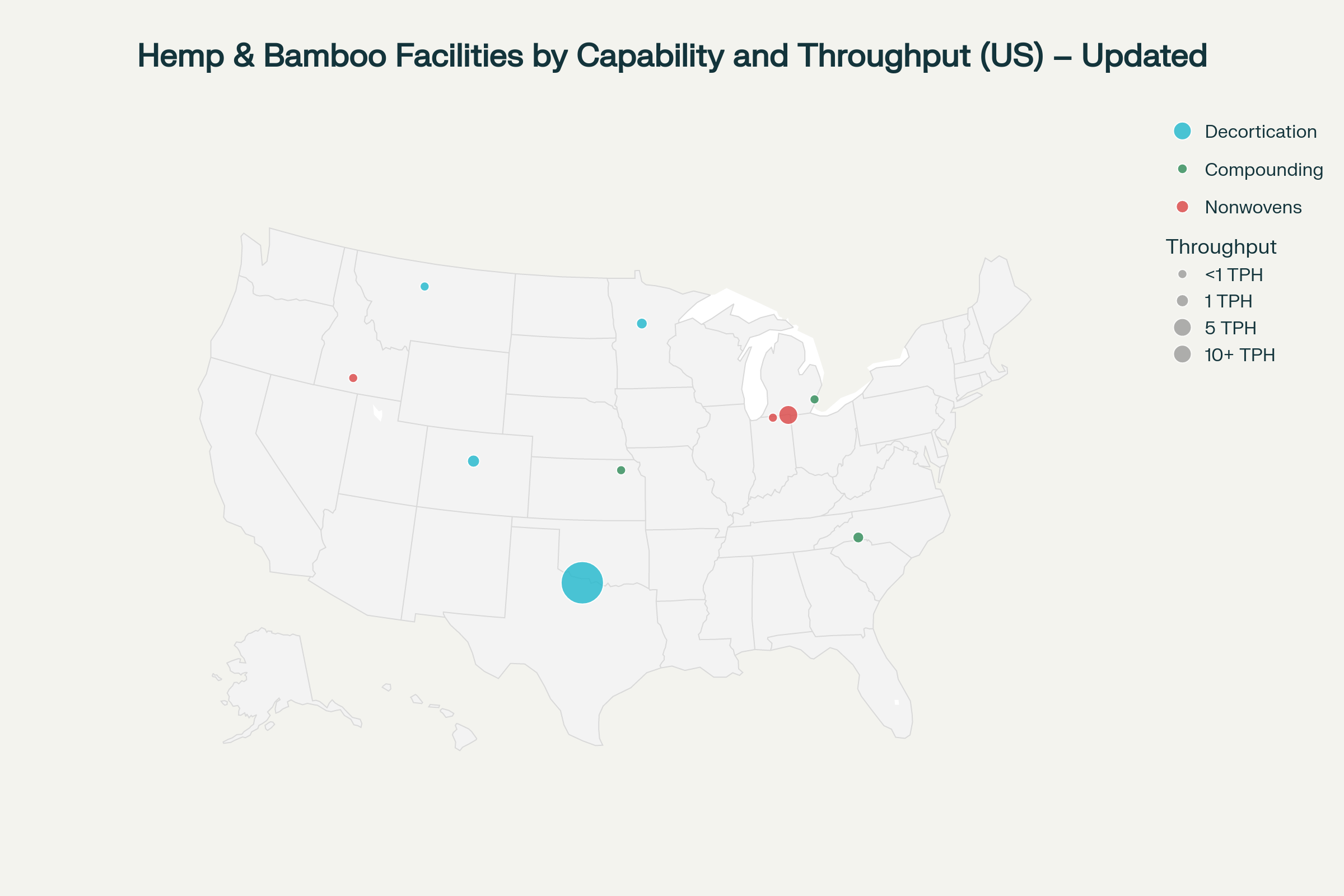

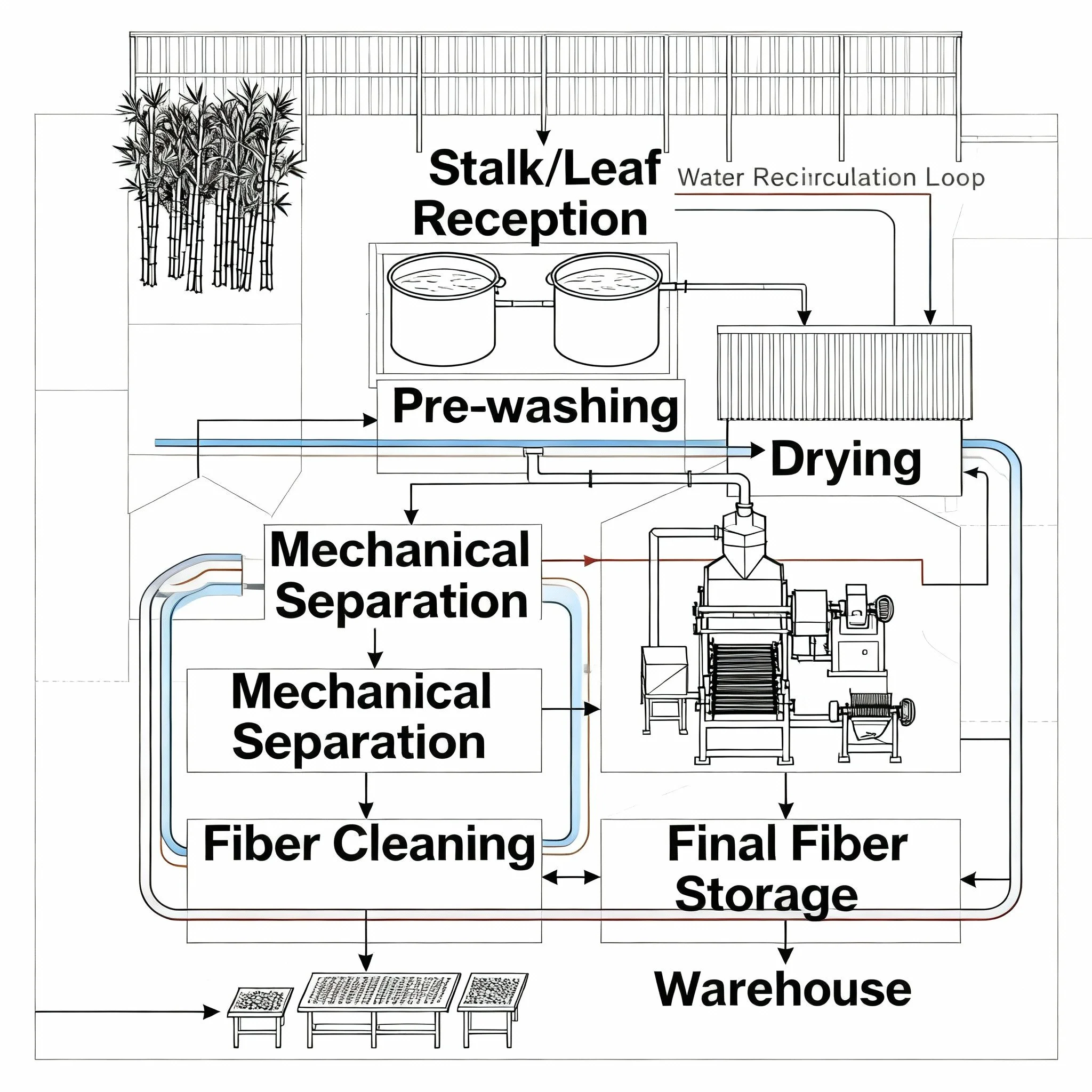

Process categories we’re mapping

Primary: decortication, chipping, pulping, retting systems, drying, fiber cleaning.

Intermediate: carding, spinning, nonwovens, compounding (PP/PLA/PHA), sheet/panel pressing, pelletizing, carbonization/activation.

Finish & Convert: weaving/knitting, lamination, molding, machining/CNC, finishing & QA.

If your line makes feedstock in, usable input out, you’re on our radar.

What we collect (operator intake)

You hate forms. Good. So do we. We only ask for what closes deals.

Capabilities

Line type(s) & make/model, current throughput (TPH/TPD) and available duty cycle

Max fiber length & spec, moisture window, tolerance stack

Current outputs (bales, tow, hurd, pellets, mats, sheets, compounds)

Constraints

Top three bottlenecks (electrical, drying, labor, QA, feedstock, offtake)

Changeover time; maintenance rhythm; QA regime (ISO/PPAP if applicable)

Scrap/waste streams & reuse potential

Deals

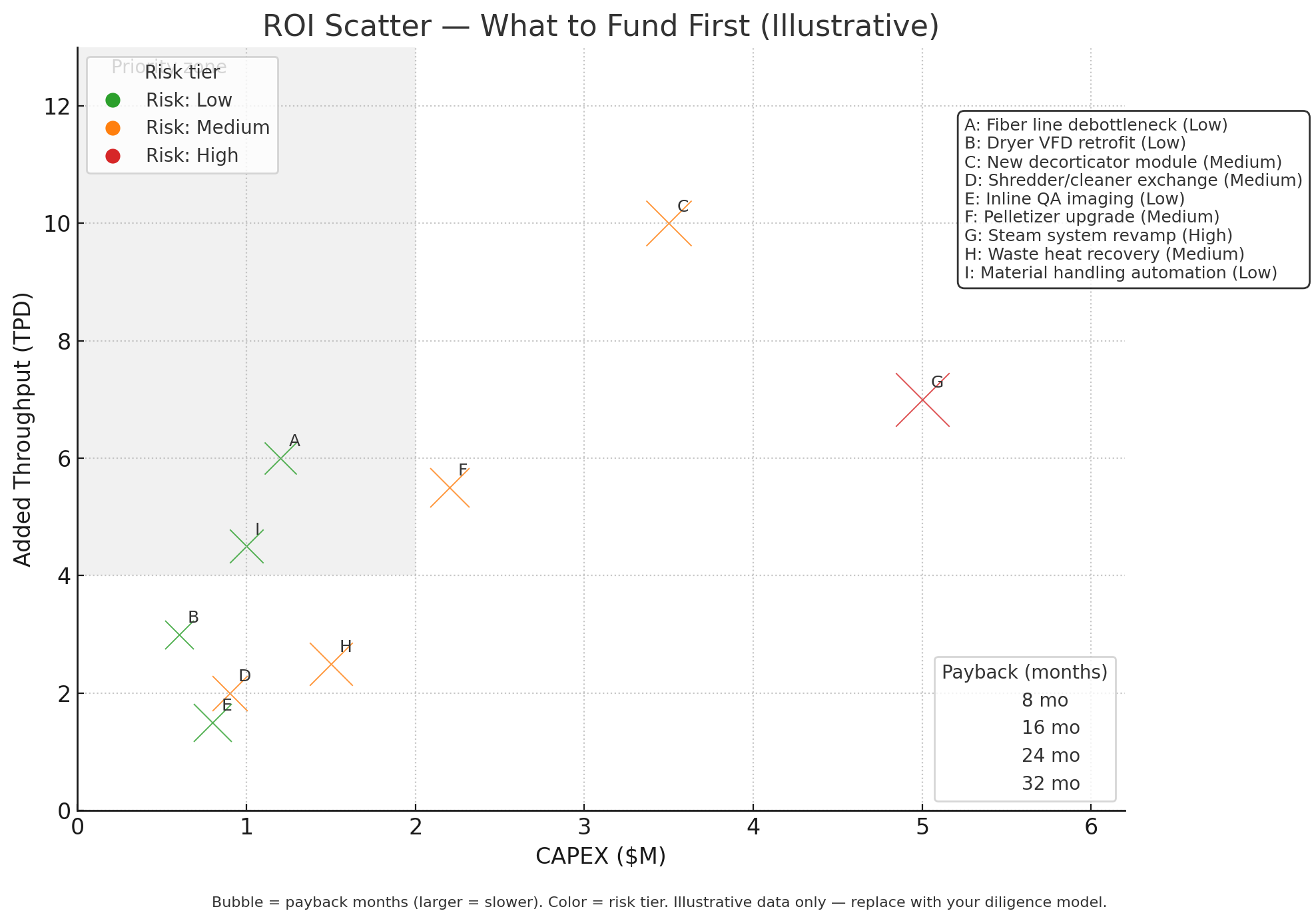

Upgrade options (good/better/best) + rough CAPEX per option

Earliest install window; vendor lead times

Offtake (existing or conditional)

Eligible incentives you’ve already scoped (we’ll verify)

Compliance & site

FEOC exposure, Domestic Content positioning, Energy Community status

Interconnect, power price, backup/DER options

Permits, zoning, environmental constraints

If you can’t disclose publicly: fine. We run a private lane until you’re ready.

What funders get (and what we expect)

A pipeline of shovel-ready upgrades with:

Unit economics before/after (not poetry)

Incentive fit (45X/48C, §6417/§6418, muni/utility stacks)

Risk register + mitigation (supply, offtake, technical, compliance)

We expect speed, transparency, and adult terms. If you need six committee meetings to underwrite a dryer, skip us.

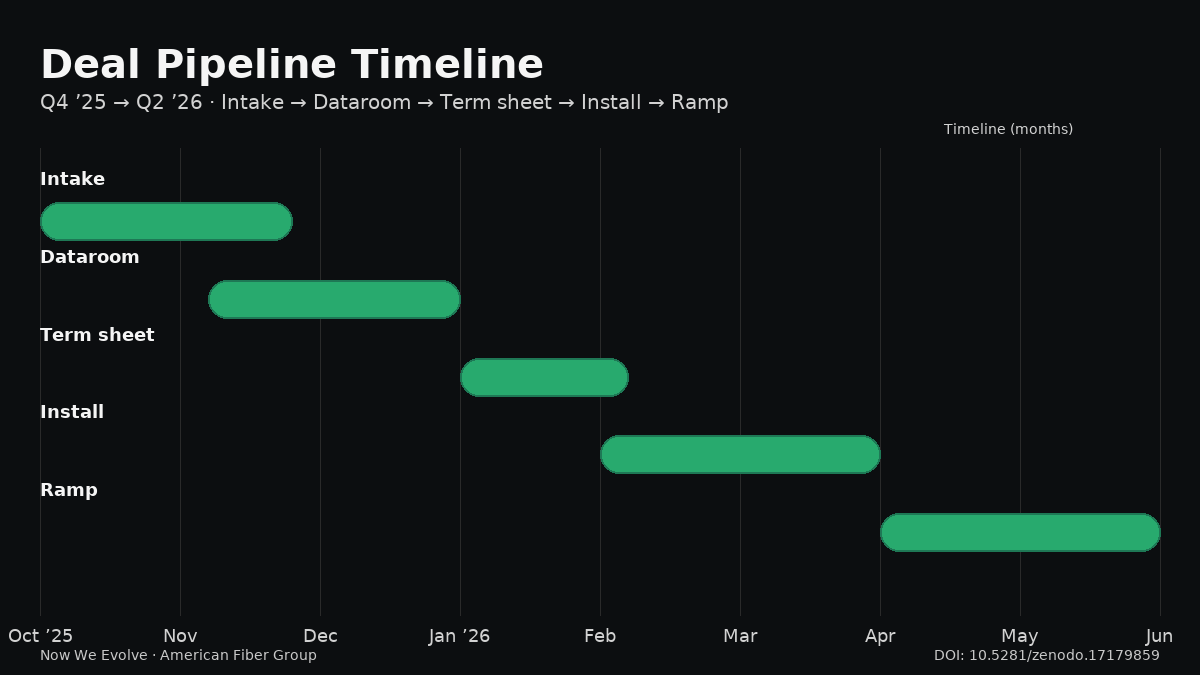

How deals will actually look (templates we use)

Throughput add-ons (dryers, mills, carders, press capacity) with transferable credits to reduce cash outlay.

Anchor offtake via big buyer MSAs, then open capacity for SMEs.

Co-locate where interconnect + waste heat + logistics line up (stop fighting physics).

Roll-up paths reserved for operators who can actually operate.

No, this is not legal or tax advice. Yes, we work with the adults who do that part.

What goes live publicly vs privately

Public Atlas (hub page):

Facility name (or anonymized regional marker if requested)

Process category, state/region, contact channel

High-level capability tags (e.g., Decortication · 3–4 TPH · Nonwovens feedstock)

Private Dataroom (case-by-case):

Detailed throughput logs, vendor quotes, capex options, QA docs, pricing bands

Deal models incorporating incentive stacks

We do not publish anything you mark private. Full stop.

How to get in (operators)

Don’t send a pitch deck. Send your three ugliest problems.

Email: eric@americanfibergroup.com with subject AFG Intake – <Company – Line Type> and a 7-bullet email:

Site & line(s)

Current throughput & run schedule

Top 3 constraints

Upgrade options (+ ballpark CAPEX)

Install window & vendor lead times

Offtake status (actual buyers, not “in talks”)

Compliance notes (FEOC/DC/Energy Community)

If it’s obviously real, we book a 30-min ops call and start packaging the upgrade.

How to get in (funders)

Email: eric@americanfibergroup.com with subject AFG Capital – <Fund – Check Size> and include:

Check size, target IRR, risk appetite

Timeline from first call to term sheet

Appetite for §6417/§6418 & 45X/48C structures

Any “never touch” constraints

If you need a beauty pageant, we’re not your shop. If you want first-mover dealflow, let’s go.

FAQ (blunt)

Q: Are you taking public contributions?

A: Not right now. This isn’t Wikipedia; it’s a deal machine. DM or email.

Q: Are bamboo processors included?

A: Yes. If it moves lignocellulosic fiber toward a real product, we care.

Q: Can universities participate?

A: If your lab produces industrial inputs and can hit a delivery window, absolutely.

Q: What about international processors?

A: We start with North America. If a cross-border link solves a US bottleneck without FEOC problems, we’ll consider it.

Call to action

Operators: send us your bottlenecks, not your branding.

Funders: bring terms, not platitudes.

Customers: tell us the spec you’ll sign for—we’ll route fiber to it.

Email: eric@americanfibergroup.com

Cite the spine: DOI 10.5281/zenodo.17179859

Repo: https://github.com/EvolutionMine/thewall

Read the full story in the book.

Evolution Mine: The Industrial Evolution—the blueprint for breaking the petrochemical playbook and building a regenerative economy.

👉 Buy on Amazon